To illustrate why I made the point that the appliance market generally and service is changing and that China is quickly becoming a major threat to legacy brands, let’s look at one many if not most people know about, cars.

Prior to 2024 Chinese-produced vehicles in the UK (and most of Europe) were little more than a curiosity; there were a few, but they were very limited and widely regarded as, will we say, not great.

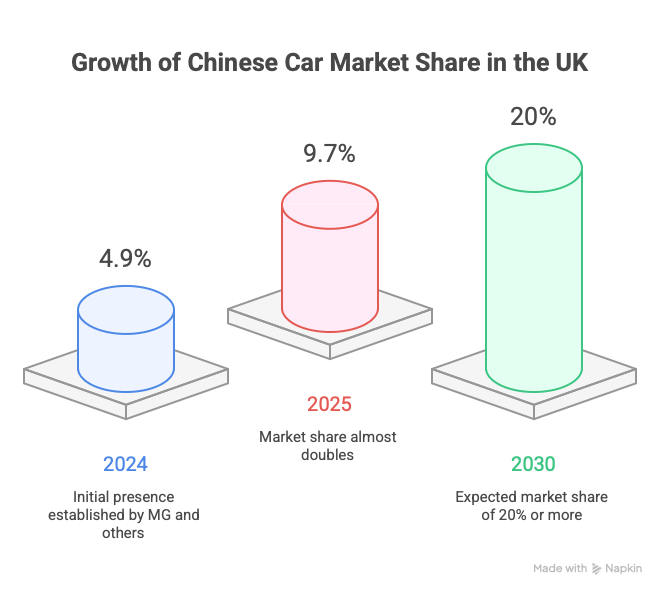

In 2024, after MG (SAIC) and a couple of others had established a presence that suddenly became 4.9% of the UK market.

In 2025, that almost doubled to 9.7%.

By 2030, it is widely expected that Chinese brands or owned brands will account for 20% or more of the UK market.

That’s a fifth of the market and, a fifth of the market that the incumbent manufacturers have lost, and now they are fighting harder for a smaller market share.

They will struggle to combat the more keenly priced Chinese products using an argument on quality because the Chinese-made vehicles are on a par with many of the volume brands, some knocking on the heels of the premium players.

So that leaves the traditional brands with some tough choices, with many taking the “if you can’t beat ‘em, join ‘em” approach and partnering with Chinese companies.

There are a myriad of reasons for this, and mostly, that all makes total sense, but appliances are a little different. But it’d be naive to think they were wildly different.

Steamrollered

Many of the Chinese brands that were largely laughed at for quality and so on just a few years ago, notably Haier, Hisense and Midea, haven’t just entered the European and UK markets under their own brands; they’ve also gained massive market share through the acquisition of traditional brands we all know and love.

Hoover, Candy, Gorenje, Asko, Kuppersbusch, Teka, Delonghi, Fisher & Paykel… the list goes on and on. But I used those names for a reason, to demonstrate that the Chinese are no longer just looking at low-end mass market machines, on no, they’re very much targeting all sectors right now to the very top of the market.

And by buying up those brands, they’ve bought the expertise and rights to challenge virtually anyone.

You see the same in the automotive sector, MG, Volvo, Lotus, SAAB, Smart etc if not to the same extent, but the same tactics.

Then there are brands that do or, at least, believe they have the cache to go it alone with their own branding, like Xiaomi.

Just as we see with Deepal, Xpeng, BYD and more.

My point is, the Chinese brands by whatever route are hungry, show no sign of letting up and seem to have no issue with steamrolling the legacy brands either through acquisition or, just putting them out of business.

Panic?

This is why organisations like AMDEA and APPLiA are going nuts. Like most political things, watch what they do, perhaps not so much what they say.

What they’re trying to do is make it so EU manufacturing (and yes, they include Turkey in that, go figure) is front and foremost, promoting the fact that the sector employs about a million people and so on, you get the idea.

They’re good at what they do and are making a number of very valid points to EU authorities even if I don’t agree with all that they say, especially on service and spare parts.

Whilst all they do might not stop the advance of China I the sector, they might at least slow it down.

Service Changes

As I mooted in a previous article, this huge shift is likely to bring about changes to the appliance service sector.

Not so much automotive as that is different for vehicles, it’s not in-home service!

But, if the legacy EU brands loose 20% of their business, which is entirely possible if not very likely (perhaps more) then their requirement for service will also decrease. That’s a problem for them, where they run their own repair services.

You then have to think, at what point does running your own service become unviable?

And then, what do you do about it if it becomes no longer viable?

On top of that, the UK is (as usual) “different” to the rest of Europe from all I can learn. I always recall service managers etc at Candy not being worried about the acquisition of Hoover because they said, Candy didn’t employ repair techs anywhere in Europe so, Hoover Service in the UK would likely be shut down and all the work go to the existing service agents.

That didn’t happen.

The scuttlebutt was that Candy didn’t want to pay the redundancy to scrap the Hoover side so they tried to have some sort of mashed-up hybrid service thing going on. After a while, they sussed that it didn’t work.

Although I have nothing to support it other than anecdotal evidence, the reason was the volumes to agents dropped; they got all the garbage work, recalls, hard stuff and so forth, so many of them told Candy to get lost. It wasn’t worth the hassle.

Although I can tell you about my experience after working with Candy for many, many years.

At the end, all we got (NWAR) was gas, refrigeration (system), and problem calls that their own guys couldn’t fix so I said that the rate would have to reflect that; it wasn’t volume rates, as we weren’t getting volume. Candy wouldn’t pay any more than the paltry volume rate, which was well outta date in any event, so I politely declined to do any more work for them.

What they did after that, I’ve no clue.

That’s a real-world example of what can happen and how it can go wrong to show how manufacturers have to be careful in order to retain good service agents. Because if they’re good, they will also be good enough to know when to walk away.

Service is always changing though, it’s just the way it goes, as I explained in the previous article and some of the drivers of change.

Reading The Tea Leaves

Going forward, I’d expect more changes. I suspect some things nobody will be able to foresee; it’s a case of “best guess” based on information we have, historical stuff and plain old human nature.

As I said, it’s always changing… sometimes fast, sometimes slowly and the UK is not the EU (it never was) and doesn’t operate the same way.

The next few years could prove to be very interesting indeed.